Navigating Financial & Family Law Disputes

Law shouldn't be a maze. Whether you are dealing with a cheque bounce case or a complex family dispute, I break down the legal logic so you can take the next right step.

I discuss the alarming and growing trend of misusing stringent laws like POCSO to settle scores in matrimonial disputes. This is a serious issue that follows the historical misuse of Section 498A, as even acknowledged by the Supreme Court.

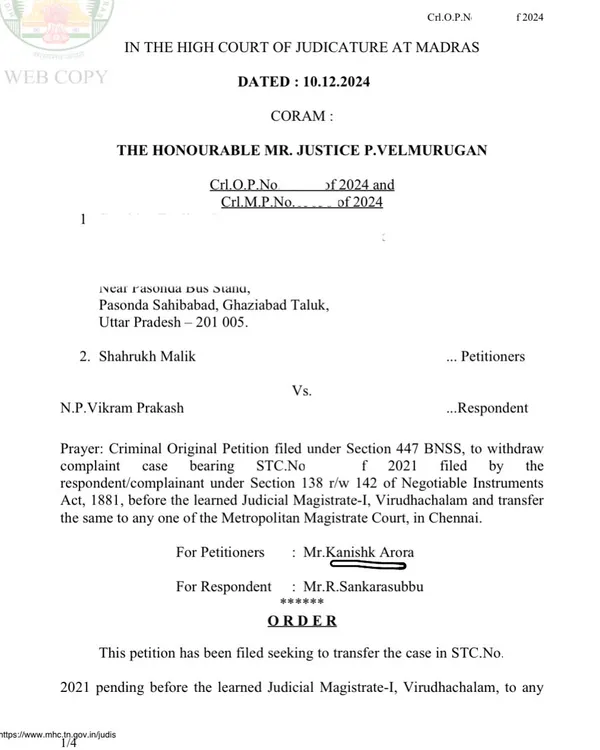

In a Section 138 NI Act case, the credibility of a witness is paramount. If a witness admits during cross-examination that they lack personal knowledge of the transaction, their testimony or affidavit loses significant value, potentially weakening the entire case.

In child custody battles, the child's welfare is the paramount consideration. I discuss an interesting Supreme Court case where both parents were convicted of murder, and the court had to decide the custody of their three children based on this principle.

In property disputes, what happens if a party sells the property while the case is pending? I explain the doctrine of 'lis pendens' and the role of interim stay orders under Order 39 in protecting the rights of all parties involved.

Does a broken promise of marriage always amount to rape? The Supreme Court has clarified the test: it is only considered rape if the man's intention was deceitful from the very beginning, solely to obtain consent for sexual activity.

Do you need a money lending license for a private loan? If you are in the business of lending money at interest, yes. An unlicensed professional money lender cannot file a case under Section 138 NI Act for a bounced cheque.

There are three main types of loans: bank loans, loans from private financiers, and friendly loans. I explain the differences and how the requirement for a money lending license can impact the validity of a cheque bounce case under Section 138 NI Act.

In cheque bounce cases, 'liability' or 'dendaari' is the core issue. This liability can arise from various transactions, such as a loan, sale of goods, advance for services, or a settlement agreement. Understanding the origin of the liability is key to the case.

Many people lose cheque bounce cases despite having a signed cheque. The offense under Section 138 NI Act is highly technical, and there are numerous loopholes that can be used as a defense, even if the accused filled out the cheque themselves.

This video revisits the concept of liability under Section 138 NI Act, focusing on the presumption of liability and how the requirement of a money lending license for professional lenders plays a crucial role in determining if a case is maintainable.

About Navigating Financial & Family Law

Don't assume a signed cheque guarantees a win in a Section 138 case. The law is highly technical, and factors like who actually signed the cheque, whether you are dealing with a joint account, or the status of the lender as a professional financier versus a friend, can completely shift the outcome of your case.

Understanding the Logic Behind the Dispute

Legal trouble rarely comes in isolation. In my 20 years of litigation and 1500+ cases, I have seen how people often get caught in the details, missing the actual legal framework that decides their fate. My approach is to strip away the jargon and focus on the core problem.

Section 138 NI Act: More Than Just a Bounced Cheque

People often believe that if they have a signed cheque, the case is won. This is a dangerous misconception. The Negotiable Instruments Act is technical. I help clients navigate:

- Liability (Dendaari): Understanding the origin of the transaction—was it a loan, a sale of goods, or a settlement? If the origin of the liability is flawed, the case can collapse.

- Jurisdiction: Don't let banks or institutions harass you by filing in remote locations. Supreme Court rulings now clarify that jurisdiction lies where your bank’s main branch is, not where the cheque was deposited.

- The 'Relevant Point of Time': In company cases, omitting specific averments about who was responsible at the time of the offence can lead to cases being quashed entirely.

Navigating Family & Matrimonial Crises

Family law requires a different kind of precision. Whether it is a child custody battle where the child's welfare is the only paramount consideration, or cases involving the misuse of laws like Section 498A or POCSO, the stakes are deeply personal. I focus on:

- Evidence & Procedure: How to present your story logically in court, rather than emotionally.

- Strategic Defense: When faced with false allegations, understanding the legal test for 'intent' and 'deceit' is crucial for your protection.

Law is about logic, and I am here to help you apply that logic to your specific situation.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

Cheque Bounce and Banking Dispute Legal Solutions

4

4

Financial Dispute Resolution Services in Delhi NCR

Practical Legal Expertise in Cheque Bounce, Labour, and Family Disputes

5

5

Legal Support for Cheque Bounce and Money Recovery

6

6

Complex Civil & Financial Litigation

Cheque Bounce: A Practical Legal Guide

More from Practical Legal Training & Coaching by Sharad Bansal

More services by Sharad Bansal