Cheque Bounce: A Practical Legal Guide

A bounced cheque isn't just a financial headache; it's a legal issue that demands immediate, precise action. Whether you're the receiver or the issuer, understanding the timelines and your rights is your best defense.

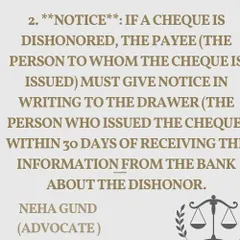

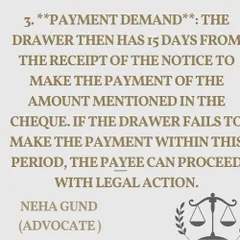

If you've received a bounced cheque, time is of the essence. I outline the step-by-step legal procedure you must follow, from sending the demand notice within 30 days to filing a complaint in court. Following these timelines under Section 138 of the Negotiable Instruments Act is crucial for a successful case.

A bounced cheque can disrupt your business, but the law is on your side. I break down the immediate actions you must take when a cheque bounces, including the strict timelines for sending a legal notice under the Negotiable Instruments Act. I also touch upon how you can claim interim compensation to get partial payment quickly.

Did you miss the 30-day deadline to send a legal notice for a bounced cheque? All is not lost. I explain the alternative legal remedies available, such as re-depositing the cheque if it's still valid or filing a civil suit for money recovery.

The details in your legal notice for a cheque bounce are critical. If you fail to include specific information about the cheque and the transaction, the court may not consider it a valid demand. I explain what must be included to ensure your notice is legally sound and your case stands strong.

If you receive a legal notice for a bounced cheque, you must respond. Ignoring it leads the court to assume you were aware of the issue and chose not to act, which can severely weaken your defence. I explain why a timely response with your side of the story is essential.

If you are facing a cheque bounce case, there are several possible defences you can use. I discuss three major grounds for acquittal, including finding contradictions in the complainant's story, questioning their financial capacity to lend the money, and proving the signature on the cheque is not yours.

If you are a partner or director in a company and have been named in a cheque bounce case, you may not be liable. I explain the grounds based on a Supreme Court judgment where you can get the case against you quashed if you had no involvement in or knowledge of the transaction.

A complainant in a cheque bounce case can ask for up to 20% interim compensation, but the court doesn't grant it automatically. I discuss the legal loopholes and grounds you can use to challenge this, such as your economic capacity and the plausibility of your defence.

Recovering a friendly loan given in cash can be difficult without proof. However, a recent Supreme Court judgment has made it easier. I explain how a security cheque, combined with proof of your financial capacity through your ITR, can help you successfully file a cheque bounce case and get your money back.

Was the bounced cheque you issued meant as a security deposit and not for an existing debt or liability? This is a crucial distinction. I explain how a security cheque can be a valid defence in a Section 138 case, and how we can argue this in court to protect you.

About Cheque Bounce: Your Complete Guide

If you have received a bounced cheque, the 30-day clock starts ticking the moment you get the return memo from your bank. Sending a legal notice is not just a formality, it is the foundational document that must contain every specific transaction detail to be admissible in court. Missing this window, or failing to detail the debt accurately, can lead to your case being dismissed on technical grounds before a trial even begins.

Understanding Section 138 of the NI Act

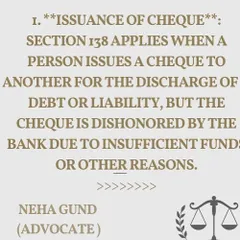

When a cheque is dishonoured due to insufficient funds, Section 138 of the Negotiable Instruments Act, 1881, becomes your primary recourse. This is a criminal provision, but it is highly procedural. The process starts with a 'demand notice' sent within 30 days of receiving the return memo.

Why the Legal Notice Matters

Many people think a notice is just a letter. In court, it is the most crucial piece of evidence. If you fail to mention the exact amount, the cheque number, or the reason for the transaction, the court may rule that no valid demand was made. This is where most cases falter at the filing stage. Do not ignore a received notice, either. If you receive one, you must respond immediately with your version of the facts; silence in court is often interpreted as an admission of liability.

Building Your Defense

If you are on the receiving end of a case, an acquittal is not impossible. We look at three major pillars of defense:

- Contradictions: Checking the complainant's claims against their own evidence.

- Financial Capacity: If the amount is large, did the complainant actually have the capacity to lend that money?

- Signature & Authenticity: Was the cheque actually issued for a debt, or was it a blank security cheque misused later?

The Risk of Ignoring Court Dates

Court proceedings for cheque bounce are strict. Even if you are innocent, failing to appear or missing dates can lead to non-bailable warrants. If you cannot attend, your counsel must represent you at every hearing. My focus is on ensuring your documentation is precise and your presence (or representation) is consistent to avoid these unnecessary technical losses.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

Cheque Bounce Recovery: Legal Steps & Defense

Legal Strategy for Cheque Bounce & Financial Disputes

Cheque Bounce and Banking Dispute Legal Solutions

5

5

Legal Support for Cheque Bounce and Money Recovery

4

4

Financial Dispute Resolution Services in Delhi NCR

Legal Solutions for Financial Disputes & Money Recovery

More from Commercial Litigation & Dispute Resolution by Karan Sharma