Protecting Your Personal Assets from Business Liabilities

Your business signature should not cost you your home. If you have signed as a personal guarantor, your family assets are exposed to banking recovery laws. Let's look at how to legally separate your company's debts from your private life.

Signing a guarantee is not "just a formality." It can make you 100% liable for the full loan plus interest, and verbal promises from banks are worthless. Ignoring notice letters is one of five deadly mistakes that can destroy family wealth.

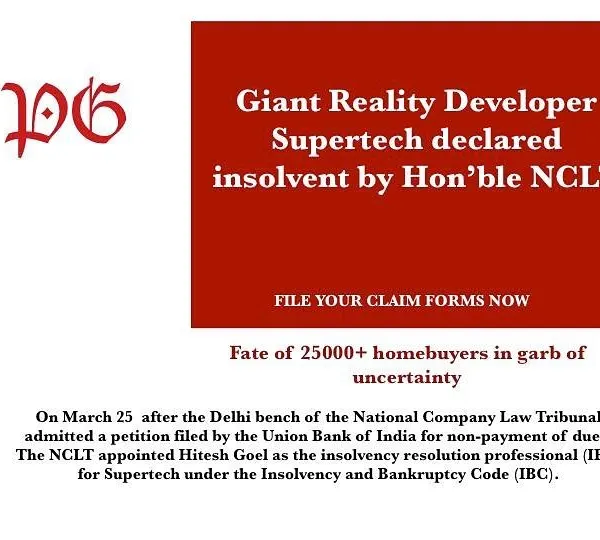

A real NCLT Bengaluru case involved the seizure of a guarantor's personal home despite business insolvency. Your personal guarantee makes your wealth repayable, and any asset, including inherited property, can be targeted.

About Protecting Personal & Family Wealth

Many business owners mistakenly believe that if their company enters the NCLT process, their personal home or joint accounts are automatically shielded. They are not. If you have signed a personal guarantee, the bank views your entire net worth as repayment capital. You need to verify immediately if your guarantee deed contains a specific limit of liability clause; if it does not, your entire personal asset base is technically up for grabs unless you restructure your legal standing.

The Personal Guarantee Trap

When you signed that loan agreement, it likely included a personal guarantee. Banks present this as a formality, but under the Insolvency and Bankruptcy Code (IBC), this signature effectively removes the corporate veil. It gives creditors the right to pursue you personally for company defaults. We have seen clients lose homes, cars, and even inheritances because they assumed the company structure would protect them.

Why You Must Act Before the Notice Arrives

Waiting for a demand notice from the DRT or NCLT is the most dangerous strategy you can adopt. By the time a notice arrives, the bank has already prepared their filing to attach your assets. We focus on pre-litigation strategies:

- Guarantee Audits: We review your loan documents to identify clauses that might be legally unenforceable or procedurally flawed.

- Liability Capping: We help you negotiate with lenders to legally cap your personal exposure before the situation escalates to tribunal filings.

- Asset Ring-Fencing: We create legal firewalls to ensure family assets remain distinct from business accounts.

Challenging the Bank

Not every personal guarantee holds up in court. Banks often fail to follow strict disclosure norms or provide adequate explanations of risk at the time of signing. We help you use these procedural lapses to challenge the validity of the guarantee itself. Whether it is resisting an insolvency petition or filing for a stay order on property auctions, our objective is to buy you time and reduce your personal liability.

Your Second Chance

The law is meant to be a tool, not a weapon. If you are already under pressure, our goal is to turn your financial mess into legal clarity. We do not promise miracles, but we do provide a clear-eyed assessment of your litigation risk and a roadmap to save what you have built.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

6

6

Navigating Debt and Financial Disputes

Banking & Finance Law Explained

4

4

Navigating Insolvency and NCLT Proceedings for Homebuyers

Understanding Your Rights as a Consumer

13

13

Financial Clarity and Legal Rights Before Marriage

Insolvency and Bankruptcy Law Litigation

More from Corporate & Insolvency Law by Ramniwas Surajmal

More services by Ramniwas Surajmal