Defending Your Rights at the Debt Recovery Tribunal

A DRT notice is not the end of your financial journey. It is a time-sensitive legal process where your response determines the outcome. We help you challenge bank claims, stop wrongful auctions, and protect your assets.

The Debt Recovery Tribunal in Bangalore is not just for banks. We have helped clients freeze wrongful property auctions, reduce liabilities by 40 to 50 percent through legal negotiations, and win moratoriums. If banks can use the DRT, so can you.

The Karnataka High Court has ruled that the DRT cannot extend the 45 day appeal deadline under the SARFAESI Act. There are no second chances. Missing this window means your case could be lost. We ensure you act on time.

This post highlights recent Bengaluru DRT updates that borrowers must know, covering new rules, digital notices, and the risk of delayed hearings. We help you navigate these changes to your advantage.

Our team is ready to assist if you have received a DRT or SARFAESI notice. We help borrowers stop auctions, file objections, and protect their property legally before it is too late.

The DRT in Bengaluru has shifted locations, causing many borrowers to miss hearings and face ex-parte orders. We help you track your calendar, confirm venues, and file recall applications if needed.

A Karnataka High Court ruling states that releasing one co-surety does not release others. If you are a guarantor, your liability remains. We review your documents and help you file for contribution if you have paid more than your share.

The Supreme Court has ruled that the DRT cannot declare sale deeds illegal. If your property was sold unlawfully under SARFAESI, you must file a civil suit. We help build a parallel DRT and Civil Court strategy for you.

This infographic introduces the top five borrower rights in DRT cases that you might not know. Knowledge is power, and we believe in empowering our clients to fight smartly and confidently.

Your first right in a DRT case is the right to be heard before any action is taken. Banks cannot proceed without giving you a legal hearing. We ensure your voice is heard.

Your second right is to receive proper notice. We scrutinize every notice for procedural flaws, as errors in the bank's process can be a strong point in your defense.

About Your Defense at the Debt Recovery Tribunal (DRT)

The biggest mistake I see borrowers make is replying to a DRT notice with an emotional letter to the bank manager. That is not a legal defense. Banks operate on procedural strictness. If their notice has a minor clerical error or misses a statutory timeline, that is your opening. Before you send any response, ensure we audit the NPA classification and loan documents first. A single technical flaw can be the difference between keeping your property and losing it to a forced auction.

Receiving a notice from the Debt Recovery Tribunal (DRT) feels like the walls are closing in, but the law provides specific tools to push back. The DRT is not just a place for banks to recover dues; it is a forum where your defense matters. Under the SARFAESI Act, banks must follow a rigid procedure. When they fail—whether by issuing an improper notice, miscalculating the NPA date, or skipping mandatory valuation steps—the entire recovery process can be challenged.

Why Your Initial Response Matters

Many clients come to us after they have already inadvertently admitted liability through poorly drafted replies. A SARFAESI 13(2) notice is not just a letter; it is a statutory trigger. If you do not file a formal Section 13(3A) objection, you lose your right to contest the bank’s claims later. We meticulously audit your account against RBI IRAC (Income Recognition and Asset Classification) norms to see if the bank’s NPA tagging is even valid.

Our Strategic Approach

- Stopping Auctions: If you are facing an imminent property auction, we file Section 17 applications in the DRT to seek an immediate Stay Order.

- Procedural Defense: We look for lapses in notice affixation, valuation errors, or non-compliance with the Securitisation Act.

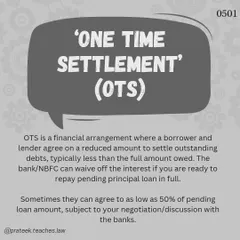

- Negotiation over Litigation: Sometimes, a One-Time Settlement (OTS) is the smartest exit. We handle the intense negotiations with Zonal Managers to secure debt closure at a discount, ensuring you get a clean No Dues Certificate without hidden liabilities.

- Guarantor Protection: If you are a director or personal guarantor, your assets are in the crosshairs. We challenge the invocation of personal guarantees, especially when the principal borrower's case is still in dispute.

Don't let the 45-day appeal window or the 60-day SARFAESI clock run out. Time is the most expensive commodity in a DRT case.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

6

6

Navigating Debt and Financial Disputes

Legal Solutions for Financial Disputes & Money Recovery

4

4

Financial Dispute Resolution Services in Delhi NCR

Insolvency and Corporate Restructuring Legal Services

4

4

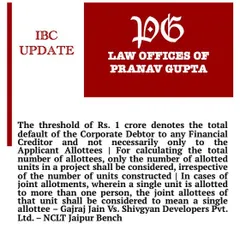

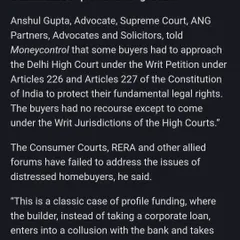

Navigating Insolvency and NCLT Proceedings for Homebuyers

Legal Help for Trapped Homebuyers in Subvention Schemes

More from Debt Recovery & Banking Law (Borrower Defense) by Ramniwas Surajmal

More services by Ramniwas Surajmal