Lessons from High-Profile Corporate Debt Cases

Understanding how major corporate debt crises unfold can save your personal assets. We analyze the legal missteps in high-profile cases so you know exactly how to handle your own banking notices.

Vijay Mallya's claim of being declared a willful defaulter without a chance to respond is a reminder of the risks under the IBC. The law is not the enemy, but its misuse is. We help clients navigate complex IBC matters with fairness and clear legal strategies.

"Before I was heard, I was judged." This quote from Vijay Mallya is a reminder for every borrower. The story that shook India's financial scene holds valuable lessons on transparency and legal compliance.

The first mistake in the Mallya case was a lack of transparency. His empire began collapsing when lenders realized a lack of financial disclosure. The lesson is to always maintain clear, updated financials.

The second mistake was ignoring legal boundaries. Mallya was declared a willful defaulter and left the country. The lesson is to cooperate with legal authorities, as skipping due process worsens your case under IBC.

This infographic summarizes what borrowers can learn from the Vijay Mallya case. We help borrowers use loans for their intended purpose, respond to banks early, and never ignore legal notices to avoid serious trouble.

This image of our team reinforces our message: learn from the mistakes of others. We help borrowers stay compliant, restructure debt, and avoid the pitfalls highlighted by high-profile cases.

The insolvency battle involving Byju's is a wake-up call. The Karnataka High Court's order to preserve emails shows how vital transparency and documentation are. We help borrowers take proactive legal steps before debt spirals into a crisis.

This visual introduces our analysis of the Café Coffee Day case. We provide insights for borrowers based on the NCLT trends and early warning signs that emerged from this major corporate debt crisis.

What went wrong in the CCD crisis? This infographic explains how unchecked debt and missed warnings led to a 5,300 crore rupee liability and forced an NCLT filing, offering a cautionary tale for all business owners.

The CCD debt disaster could have been avoided. This post shares three critical lessons for borrowers: track debt monthly, talk to lenders early, and use IBC pre-packs as a shield to save time and money.

About Lessons from High-Profile Debt Cases

High-profile defaults are rarely about bad luck; they are usually about poor documentation and delayed legal responses. When companies like Byju's or CCD hit the headlines, the real lesson is not just about the money lost, it is about how they handled communication with lenders. Whether you are dealing with a SARFAESI notice or an NCLT filing, the difference between a resolved debt and total asset seizure often comes down to the decisions you make in the first 60 days.

The Documentation Trap: Lessons from Vijay Mallya

The primary lesson from the Mallya case is that a lack of financial transparency acts as a trigger for aggressive insolvency proceedings. When lenders cannot verify the health of a business through clear documentation, they move to declare the borrower a willful defaulter. For you, this means your loan agreements and mortgage deeds must be audited for technical flaws long before a default occurs. We examine these documents to identify unsigned pages, incorrect interest compounding, or NPA classification errors that banks often overlook.

Proactive Communication: The Byju's Case

The recent insolvency battle involving Byju's highlights how crucial internal documentation and record-keeping are during financial distress. When a company fails to preserve evidence or communicate with creditors during the early stages, the situation quickly spirals into a courtroom crisis. If you have received a SARFAESI 13(2) or 13(4) notice, silence is the worst possible strategy. Our approach is to file formal 13(3A) objections immediately to create a documented dispute on record, preventing the bank from taking unilateral possession of your assets.

Early Intervention: Avoiding the CCD Scenario

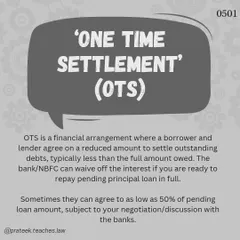

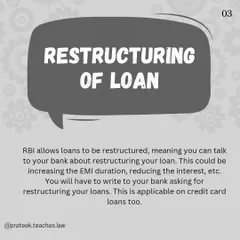

The Café Coffee Day crisis underscores the importance of restructuring debt before an NCLT filing becomes inevitable. Many business owners wait until they receive an insolvency notice to act, by which time their options are severely limited. We emphasize negotiating a One-Time Settlement (OTS) or restructuring your repayment plan while you still have leverage. Using the IBC as a shield rather than letting it be used as a sword against you is the difference between saving your business and watching it liquidate. We bring this strategic foresight to every client, ensuring you are prepared for the bank's next move.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

4

4

Landmark Insolvency Litigation & Client Victories

Insolvency and Corporate Restructuring Legal Services

Insolvency and Bankruptcy Law Litigation

Practical Legal Help for Money Recovery and Financial Disputes

6

6

Navigating Debt and Financial Disputes

Banking & Finance Law Explained

More from Debt Recovery & Banking Law (Borrower Defense) by Ramniwas Surajmal

More services by Ramniwas Surajmal