The Guarantor's Trap: Protecting Your Assets

You signed as a guarantor to help a friend or business, but now your own assets are at stake. A single signature can turn your personal savings and home into collateral for debts you did not even accrue. We help you isolate your personal liability before the bank claims ownership.

This visual from our Real Estate Law Series exposes the hidden GPA trap. A property paper you signed as a "witness" years ago could be used by banks today to destroy your financial stability.

A Bangalore techie lost his 2.8 crore rupee apartment because he signed as a witness on his uncle's property deal. This infographic debunks deadly GPA myths and explains how old papers never expire.

This is from our IBC Warning Series for Borrowers. It cautions company directors that their personal assets are not safe from creditors, a fact many business owners overlook.

Our IBC Warning Series starts with a critical alert for guarantors. A doctor's wife lost her ancestral home over her husband's business loan guarantee. Your signature can put your family's wealth at risk.

About The Guarantor's Trap: Protecting Your Assets

Many guarantors assume their liability is limited to the principal loan amount, but most modern banking contracts include 'unlimited liability' clauses that few read until it is too late. If you have been issued a notice under the SARFAESI Act, you have a 60-day window to legally contest the NPA classification and the validity of the guarantee itself. Do not wait for the bank to issue a possession notice for your property.

Understanding Your Liability

Being a guarantor is often presented as a simple favor or a formality, but legal reality tells a different story. Banks frequently bundle these guarantees with 'unlimited liability' clauses. If the borrower defaults, the bank can legally pursue your personal savings, joint accounts, and even your ancestral home to recover the debt.

The 60-Day SARFAESI Window

If you have received a notice under Section 13(2) or 13(4) of the SARFAESI Act, the clock is ticking. You have a limited statutory window to act. We focus on these specific actions:

- Forensic Audit of NPA Classification: Banks often classify loans as Non-Performing Assets (NPA) prematurely or incorrectly. We audit the loan statement against RBI IRAC norms to challenge this classification.

- Challenging the Guarantee: We review the original loan agreement to check for procedural lapses, such as unsigned pages or outdated Power of Attorney documents that might invalidate your guarantee.

- Stay Order Filing: If a property auction is imminent, we file applications in the Debt Recovery Tribunal (DRT) to secure a stay order, halting the recovery process while we contest the bank's claims.

Why Act Now?

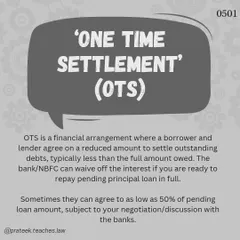

Ignoring a notice does not make the debt go away; it only reduces your legal leverage. We have represented clients in Bengaluru and across India who were initially told by banks that they had no recourse. By identifying the specific technical flaws in the bank's recovery process, we negotiate from a position of strength, aiming for a One-Time Settlement (OTS) or a total release from the guarantee. Your signature is not a blank check for the bank. Let us help you review your legal position before the bank takes further action.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

6

6

Navigating Debt and Financial Disputes

Banking & Finance Law Explained

Practical Legal Help for Money Recovery and Financial Disputes

Essential Legal Steps for Cyber Fraud Recovery

Legal Help for Trapped Homebuyers in Subvention Schemes

4

4

Navigating Insolvency and NCLT Proceedings for Homebuyers

More from Debt Recovery & Banking Law (Borrower Defense) by Ramniwas Surajmal

More services by Ramniwas Surajmal