Important Income Tax Filing Deadlines and Alerts

Missing a tax deadline triggers immediate penalties and interest charges. Stay ahead with our expert guidance to ensure your filings are always compliant and on time.

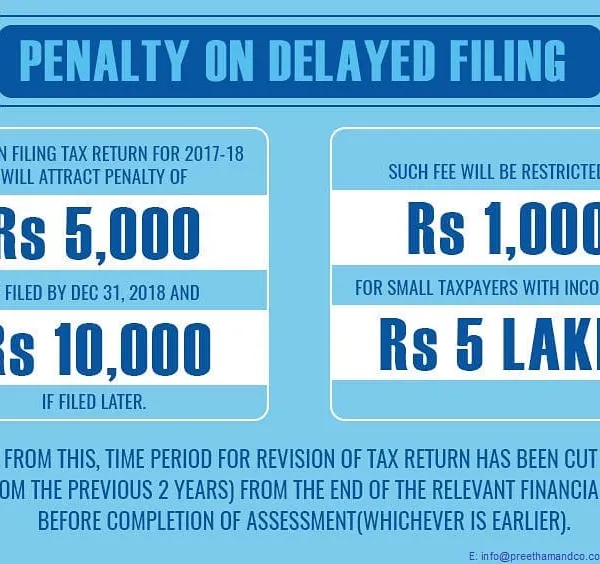

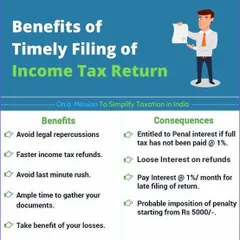

Filing your ITR by the 31st July deadline is crucial to avoid a cascade of negative consequences. As this graphic shows, late filing can result in penalties under section 234F, interest payments, and the inability to carry forward losses. We manage this process to protect you from these costly and unnecessary outcomes.

To reinforce the importance of timely filing, this alert details the specific issues that arise from missing the 31st July deadline. These include financial penalties, a reduced timeframe for revising your return if an error is found, and delays in receiving any tax refunds you are owed. Our service is designed to prevent these exact problems.

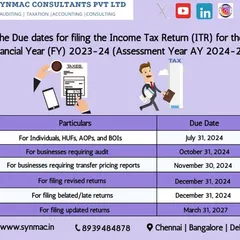

For salaried individuals and other specified taxpayers, the 31st July deadline is the most important date in the tax calendar. We encourage early filing to avoid the last minute rush and recommend e-verifying your return for speedy processing. Filing after this date automatically attracts a late fee and interest.

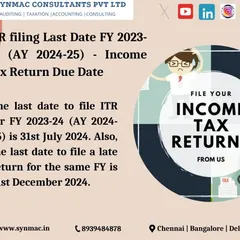

This is a final call for taxpayers who need to file their ITR for FY 2024-25 by the extended deadline of 15th September. Missing this date will lead to penalties and interest. We can help you file correctly and on time, even if you are approaching the last few days.

About Important Filing Deadlines & Alerts

Many taxpayers wait until the final 48 hours, but that is where most errors occur. Filing before the deadline is not just about avoiding the Section 234F penalty; it is about ensuring your Form 26AS and Annual Information Statement (AIS) data are reconciled correctly. If you file in a rush, you often miss out on claims or carry-forward losses you are rightfully entitled to.

Filing your Income Tax Return (ITR) is a legal obligation, but the tax department treats it as a data match. When you file closer to the due date, you lose the buffer time needed to rectify discrepancies between your bank statements and the tax portal’s data.

Why the deadline matters

The 31st July deadline is the standard cut-off for most salaried taxpayers, while specific business or audit deadlines follow later. If you cross these dates, the consequences are immediate:

- Penalty: Section 234F levies a fine for late filing, which can reach ₹5,000 depending on your income.

- Interest: You start paying 1% interest per month on the unpaid tax liability under Section 234A.

- Loss Carry Forward: This is often overlooked. If you file late, you lose the right to carry forward capital losses or business losses to future years, which could have reduced your tax burden in the future.

How we handle the rush

Our approach is to treat every filing as a scrutiny-proof document. We start by cross-verifying your AIS and TIS summaries against your income proofs. This identifies potential mismatches before the department does. By reconciling these early, we ensure that when your return is processed, it is flagged for a refund, not a notice. We do not just file your return; we review your financial trail to ensure you are compliant with all disclosures, including foreign assets or high-value transactions. Do not let a calendar date dictate your financial stress; get your documentation sorted early.

Similar work from other experts

Browse through Curated picks from other experts on mytribe

20

20

ITR Filing Deadlines & Expert How-To Guide

6

6

Tax Deadlines and Avoiding Late Filing Penalties

5

5

Stay Ahead of Deadlines

Income Tax Explained: Expert Filing and Compliance Solutions

20

20

Income Tax Filing Made Simple for You

6

6

Direct Tax Updates and Income Tax Filing Services in Bangalore

More from Tax Notice Response & Representation by Taxxify

More services by Taxxify